When Will Real Wages Rise in Japan?

Real wages in Japan have fallen continuously for two years. When will it end?

What would make you raise wages for your employees? If we think about wages from the perspective of an employer, perhaps we can think about how likely it is that real wages will rise in Japan in the near future.

Japan has serious labour shortages, which means companies may need to raise wages in order to attract employees or retain them. Labour shortages aside though, if you haven’t got any money to pay your employees more, you won’t be able to raise wages.

Profitability

You’re going to need rising profits out of which to increase your employees’ pay. Are profits rising in Japan? Yes, they are: corporate profits were rising slowly and steadily until the Covid emergency, and since the third quarter of 2020, they have risen at a good lick, by 51 percent. These are corporate profits averaged across the whole economy of course, so they could be skewed by say, a collection of large exporting companies assisted by a weak yen. However, according to this article from the Nikkei Asia: Japan's smaller companies gain leeway to raise pay on steady profits, even medium-size and small companies in Japan have seen profits rise by 13.6 percent in the last four years.

Even so, to ensure those higher corporate profits are actually going to be distributed to employees, it might be a good idea to look at what the profits are like for the three big employment industries in Japan: health and welfare, manufacturing and wholesale and retail.

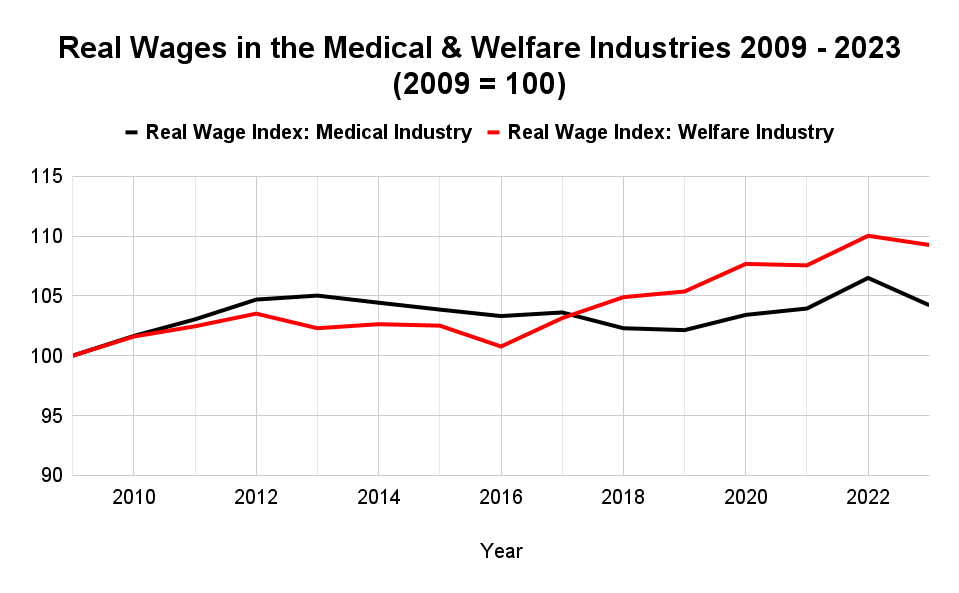

It’s difficult to find figures for profitability in the health and welfare sector, but these two articles: Number of nursing care hospital users has increased, but business conditions have worsened and General hospitals' medical profit margins are negative again, do not bode well for wage increases for medical and welfare staff. On the other hand, labour shortages are high in this sector, which could push wages up. I’m sceptical of this though, as wages in the sector haven’t risen very much over the last few years, despite the ongoing shortages:

So, the profits aren’t really there for a rise in wages in this sector, especially as medical treatment rates are regulated, and any increase in rates would necessitate an increase in medical insurance fees — robbing Kenji to pay Kento. Instead of wage rises, we’re more likely to see service cuts here.

How about profits in the manufacturing and wholesale and retail industries? They’re doing well, profits almost doubling in the two years after the Covid emergency in the manufacturing industry. At the same time, profits increased substantially for the wholesale and retail industry with operating margins remaining around the same (source METI statistics1). So manufacturing, at least, certainly has the money to splash out on pay rises.

Productivity

Profitability though, can be short-lived. If you’re going to raise wages, will profits continue to remain high? If not, you could be saddled with increased costs, but no extra profits to cover them.

Somehow, you have to believe that your future profits will continue to be higher. Something fundamental will have to shift in your industry — either higher sales, or increased productivity. Higher domestic sales with a falling population are unlikely, except for new items of technology. If you’re selling overseas, a consistently weaker yen or a growing overseas market should give you steadily increasing profits. If you’re not selling overseas though, it really comes down to productivity growth.

And the news on this front isn’t so great:

I couldn’t get data past 2020, but clearly productivity for the Health & Welfare sector has declined since 2000. Wholesale and Retail sector productivity hasn’t really changed since 2000 either. Manufacturing productivity has steadily increased. The information and communications sector was worth including as it has high productivity and an increasing share of the workforce. Construction is another bright spot, as productivity has actually increased unlike in other high-income countries.

Prediction Time

But really, there’s not many high-employment sectors with high productivity that are going to drive an increase in wages. As a result, I don’t see wages rising much faster than last year, I think they’ll rise at about the same rate of 1.3 percent. Inflation is forecast at about 1.6 percent for the next fiscal year, so real wages will fall slightly again, by about 0.3 percent.

The Nikkei’s Misplaced Optimism

The main reason for Nikkei Asia’s optimism on wages link here, is labour’s share of value at small and midsize companies falling. Companies have room to raise wages because they are currently spending less on them. The implication is that small and midsize companies have been keeping wages down, resulting in labour’s share of value falling. However, this paper from last year suggests that the labour’s falling share of value is mostly due to “declines in self-employed and SME executive labor income”. Basically, the number of self-employed (who often have a very high labour share of income) has been falling due to tax changes in the 1990s. “Salaries and bonuses to employees have hardly contributed to the labor share’s decline,” according to the paper. Indeed, the number of self-employed in Japan has fallen from 7.4 million in 2010 to 6.6 million in 2021. (source: globaldata.com)2

Therefore, small and medium-sized companies in Japan don’t have as much leeway to raise wages as the article implies.

More Misplaced Optimism

This article’s headline at Nippon.com: More than 80% of Japanese Companies Plan to Raise Wages in 2024, sounds great, until you look at the survey and realise that most companies only plan to raise wages at the same rate as in 2023:

And the number of companies that plan to raise wages at less than the rate in 2023 is higher than the number of companies that plan to raise wages more in 2024 than in 2023.

Any Grounds for Optimism?

Yes, there are, but maybe about 10 years down the road. Firstly, as we saw in previous articles, part time wages have been rising strongly. Eventually, the cost of employing part-time workers is likely to start pushing up wages more for full-time workers too. Also, in previous articles, we saw the wage profile for workers being flattened as the workforce aged. In about 10 years’ time, the 1973 baby boom pig will begin shifting out of the python, as they are currently in their early 50s. The upward shift in wages for younger workers should then begin to push up overall wages. Hopefully, in 10 years, there will also be technological improvements that will allow productivity in the medical/health and welfare industry to improve.

https://www.meti.go.jp/press/2023/01/20240130003/20240130003-1.pdf; https://www.meti.go.jp/english/statistics/tyo/kikatu/pdf/2022_Summary_of_Survey_Results.pdf

https://www.globaldata.com/data-insights/macroeconomic/number-of-self-employed-in-japan-2137691/#:~:text=2022%20Source%3A%20GlobalData-,Self%2DEmployment%20in%20Japan,in%20Japan%20decreased%20by%2011.3%25.

Thanks for another fascinating article. In general, I have to agree with your assessment, which leads to the conclusion that real wages in Japan won't rise very much in the near future.

As you suggested, it will ultimately come down to supply and demand. Even if the imbalance creates an opportunity for higher wages after another decade of demographic shifts, an influx of foreign workers willing to accept lower wages and/or the adoption of labor-saving technologies (including AI for white-collar positions), as well as the ability to outsource overseas to arbitrage labor costs, may thwart the potential for real wage gains.

Also, Japanese companies have found many ways to employ people on a part-time or temporary basis as a means of keeping wages down. I do not see this practice changing in the near to medium term, despite a concerted effort by the Japanese central government to promote full-time employment.

Anyway, thanks for your latest menu of food for thought!

Good article. One question, where do you get the 51% profit increase? Is that an estimate for the whole corporate sector, or listed companies only?